Reviewed by: Shoaib Abid

CEO, Revenue Cycle Management & Provider Credentialing Specialist

Last Reviewed: July 202

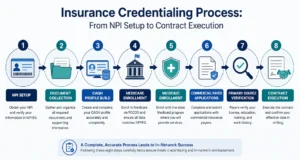

The insurance credentialing process is how a payer verifies a provider’s license, education, training, and work history, then contracts that provider into its network so claims pay at in-network rates. It runs in eight stages: NPI setup, document collection, CAQH profile build, Medicare enrollment through PECOS, Medicaid enrollment, commercial payer applications, primary source verification, and contract execution. Budget 90 to 150 days for most commercial payers in 2026. Many healthcare organizations rely on insurance credentialing services to manage these steps efficiently while integrating them with revenue cycle management services for faster provider enrollment and improved reimbursement.

What is insurance credentialing?

Insurance credentialing is the verification process a payer runs before it lets a provider join its network. The payer confirms your license, education, training, board certification, malpractice history, and work history directly with the sources that issued them. Once you pass, a separate contracting step gives you a participation agreement and an in network billing number.

Those two things get conflated constantly, and the confusion costs practices money. Here’s the distinction that matters on your first denied claim:

You can be fully credentialed and still unable to bill. That happens when the credentialing file gets approved but nobody finishes the group link, so claims come back denied because the rendering provider isn’t attached to the billing Tax ID.

What changed in credentialing in 2026?

Three shifts matter for anyone credentialing a provider this year.

NCQA compressed its verification windows. Accredited organizations now work inside a 120 day window and certified credential verification organizations inside 90 days, down from 180 and 120 respectively. Practically, that means primary source data expires faster than it used to. If you collect documents slowly, verification completed early in the process can go stale and force a partial restart.

CMS tightened cross program enforcement. A mismatch between your NPPES record and your PECOS record now creates claim denials rather than a warning letter. For the latest enrollment requirements, refer to CMS Medicare Provider Enrollment.

Continuous monitoring replaced periodic checks at several major payers. License status, OIG exclusions, and sanctions get checked on a rolling basis rather than only at initial credentialing and recredentialing. A lapsed license that used to surface at your next cycle now surfaces within weeks.

Here’s my read after watching dozens of these files move: most practice managers overrate payer relationships and underrate document hygiene. The practice with a boring, complete, correctly dated packet beats the practice with a friendly contact at the payer almost every time. Many organizations strengthen their documentation process by using insurance credentialing services to maintain accurate provider records, monitor deadlines, and reduce avoidable credentialing delays.

What documents do you need for insurance credentialing process?

You need roughly fifteen documents before you touch a single application. Gathering them after submission is the single largest cause of credentialing delay, and it’s entirely avoidable.

Provider level documents

- Current state medical license, one for every state where you’ll see patients

- Individual Type 1 NPI, with the NPPES record matching your legal name exactly

- DEA registration, current and matching your practice address, if you prescribe

- State controlled substance registration where your state requires one separately

- Board certification certificate, or documentation of eligibility status and exam date

- Medical school diploma and residency or fellowship completion certificates

- Curriculum vitae in month and year format with no unexplained gaps over 30 days

- Malpractice insurance certificate showing carrier, policy number, limits, and dates

- Malpractice claims history, including closed claims and settlements

- Government issued photo ID

- Three peer references with current contact information

- Immunization and health records where the payer or facility requires them

Practice level documents

- Group Type 2 NPI

- Federal Tax ID and a signed W-9 matching the legal entity name

- Business license and state entity registration

- CLIA certificate if you perform any in office lab testing

- Group malpractice policy, if the practice carries coverage separately from providers

- Practice address, remit to address, and correspondence address, each confirmed

The CV gap rule catches people constantly. If you took four months off between residency and your first attending role, write it down with dates and a one line explanation. An unexplained gap triggers a follow up request, and that request costs you three weeks.

How do you get credentialed with insurance companies?

Eight stages, in this order. The sequence matters more than most guides admit, because several stages depend on data created in earlier ones.

Step 1: Get your NPI and clean up NPPES

Register for a Type 1 individual NPI and, if you bill under a practice entity, a Type 2 group NPI. Then open your NPPES record and read every field against your license and W-9. Your legal name, taxonomy code, and practice address all have to match. CMS now denies claims on NPPES and PECOS mismatches, so this five minute check prevents a category of denial you’d otherwise spend months chasing.

Step 2: Build the document packet before you apply

Collect everything in the list above and scan each item to PDF. Name the files consistently. Track expiration dates for the license, DEA registration, board certification, and malpractice policy in one place. Anything expiring within 120 days needs renewal before you submit, because a payer that sees a credential expiring mid review will hold the file.

Step 3: Build and attest your CAQH ProView profile

Nearly every commercial payer pulls from CAQH. Complete the profile fully, upload your supporting documents, and then do the step people forget: explicitly authorize each target payer to access your profile. An unauthorized profile is invisible to the payer, and the application sits in limbo while you assume it’s under review.

Attest your profile every 120 days. An unattested profile reads as stale data and some payers will not proceed against it.

Step 4: Enroll in Medicare through PECOS

Do Medicare first. Commercial payers frequently reference your PECOS record, and some won’t finalize contracting without a Medicare PTAN in hand.

Individual physicians and non physician practitioners file the CMS-855I. Groups file the CMS-855B. Reassignment of benefits to a group runs on the CMS-855R. Submit electronically through internet based PECOS rather than on paper. Paper applications process substantially slower and CMS actively discourages them.

Step 5: Enroll in state Medicaid

Medicaid is genuinely state by state. Your state program has its own application, its own document list, and often requirements the commercial payers skip entirely, including fingerprinting, background checks, and site visits for certain provider categories. Look up your state’s specific requirements rather than assuming your last state’s process carries over.

Step 6: Submit commercial payer applications in revenue order

Don’t apply alphabetically. Pull your patient mix, rank payers by expected volume, and submit to your top five first. In most markets those five cover 70 to 80 percent of your potential revenue. Getting them approved months before the long tail payers is the difference between a viable first quarter and a painful one.

Some payers accept CAQH linked submission. Others require their own portal application on top of CAQH. Check each payer’s process rather than assuming CAQH covers it.

Step 7: Track verification and follow up on a schedule

Log every submission: date sent, confirmation number, assigned representative, and expected decision date. Then follow up every two to three weeks. Payer credentialing departments do not proactively tell you something is missing.

When a payer requests additional information, turn it around within 48 hours. A document request that sits for a week costs you more than a week, because your file goes back into a queue rather than resuming where it stopped. If your practice adds more than two providers a year, this tracking discipline is where the whole process lives or dies.

Step 8: Execute the contract and confirm your effective date in writing

Approval isn’t the finish line. Read the participation agreement before signing. Confirm the fee schedule, the specialty listed, the Tax ID, and the group affiliation. Then get the effective date in writing along with your in network provider number.

Do not schedule in network patients until you have that date confirmed. Services rendered before the effective date typically pay at out of network rates or don’t pay at all.

How long does insurance credentialing take in 2026?

Total elapsed time from starting document collection to your first billable in network visit runs 90 to 180 days for most providers. Here’s how that breaks down.

Notice that last row. Practices routinely forget contracting adds another month after the credentialing decision lands. If a payer tells you 120 days, your realistic first billable date is closer to 150.

One structural detail worth planning around: many payers review credentialing files only at scheduled committee meetings, often monthly. Miss the cutoff by two days and your file waits four weeks without anything being wrong with it. Ask each payer when their committee meets. It’s a question almost nobody asks, and it can save you a month.

Why does credentialing get delayed?

Five causes account for most of the damage. Many of these issues eventually result in denied claims. Learning how to reduce medical claim denials can help practices prevent revenue loss while improving overall billing performance.

Incomplete applications. Missing licenses, expired certificates, and outdated malpractice information trigger additional verification steps and push your file back in the queue.

Slow primary sources. Medical schools, residency programs, previous employers, and licensing boards all have to confirm your credentials directly. A residency program that takes six weeks to answer a verification request adds six weeks to your timeline, and you have almost no way to speed it up.

NPPES and PECOS mismatches. A middle initial in one system and not the other, or an old practice address, now produces denials rather than a courtesy correction.

CV gaps. Any unexplained break over 30 days generates a follow up request.

Multi state licensing. Every additional state license requires its own separate verification. Telehealth practices operating across five states carry five parallel verification tracks, which is why telehealth credentialing regularly lands at the long end of the range.

What does a credentialing delay actually cost?

Run the arithmetic on your own practice. A physician generating 500 encounters a month at an average reimbursement of 130 dollars represents about 65,000 dollars in monthly collections. Every 30 day delay past the expected effective date holds that revenue, and services rendered before the effective date frequently don’t get paid at all rather than getting paid later.

A 60 day avoidable delay on one provider costs roughly 130,000 dollars in postponed or lost collections. That’s the number to put in front of anyone who thinks credentialing is administrative overhead rather than a revenue function.Practices can reduce costly enrollment delays and improve cash flow by implementing revenue cycle management services alongside a structured credentialing workflow.

The cause of that delay is usually mundane. An expired DEA certificate. A CV gap nobody explained. A CAQH profile that was never authorized for the payer. None of it is complicated, which is exactly what makes it frustrating.

Not Sure Where Your Credentialing Files Actually Stand?

Chasing an application that’s been sitting in a payer queue for months drains cash flow fast. Our insurance credentialing services handle CAQH maintenance, PECOS enrollment, payer applications, and the follow up cadence that keeps files moving. We’ll review your current provider files and tell you exactly what’s blocking each one.

The insurance credentialing checklist

Work this in order. Don’t skip ahead, because later items depend on earlier ones.

Before you apply

- Type 1 individual NPI obtained

- Type 2 group NPI obtained, if billing under an entity

- NPPES record verified field by field against license and W-9

- State license current, with expiration more than 120 days out

- DEA registration current and matching your practice address

- Malpractice certificate showing carrier, limits, policy number, and dates

- CV formatted in month and year, every gap over 30 days explained

- Diplomas and training certificates scanned

- Board certification documented, or eligibility status with exam date

- W-9 signed and matching the legal entity name exactly

- Three peer references confirmed and reachable

- Payers ranked by expected patient volume

During the application phase

- CAQH ProView profile complete and attested

- Every target payer explicitly authorized in CAQH

- Medicare CMS-855 submitted electronically through PECOS

- State Medicaid application submitted with state specific requirements met

- Top five commercial payer applications submitted

- Submission log built with date, confirmation number, and contact for each payer

- Follow up scheduled every two to three weeks per payer

- Committee meeting date confirmed for each commercial payer

After approval

- Participation agreement reviewed for specialty, Tax ID, and fee schedule

- Effective date confirmed in writing

- In network provider number received and loaded into your billing system

- Group affiliation and reassignment confirmed so claims route correctly

- Recredentialing date calendared

- License, DEA, board certification, and malpractice expiration dates calendared separately

What happens after you’re credentialed?

Credentialing isn’t a one time project. Most commercial payers recredential on a two to three year cycle. Medicare revalidation runs on a three or five year schedule depending on your risk category, and CMS shortened that cycle to three years for higher risk provider types.

Separately, your license, DEA registration, board certification, and malpractice policy each expire on their own schedule. With continuous monitoring now standard at major payers, a lapsed credential gets caught quickly and can suspend your billing privileges until you fix it.

Build one calendar with every expiration date and every recredentialing date on it. Set reminders 120 days out, not 30. Renewal processes have their own lead times, and a license renewal that takes six weeks will interrupt your billing if you start it three weeks before expiration.

Attest your CAQH profile every 120 days regardless of whether anything changed. It takes ten minutes and prevents a category of problem that’s tedious to unwind. Many practices rely on insurance credentialing services to manage CAQH attestations, monitor credential expirations, and keep provider records current throughout the recredentialing cycle.

Should you handle credentialing in house or outsource it?

Depends on volume and on whether anyone owns it as a real job rather than a task squeezed between other work.

If your practice bills more than 500 claims a month and you’re bringing on a new provider this year, the honest question isn’t whether you can do credentialing in house. It’s whether the person doing it has protected time to follow up every two weeks on eight payer applications while also running the rest of their job. Usually they don’t, and the file quietly stops moving. Many growing practices solve this challenge by partnering with complete medical billing services that include dedicated credentialing support and payer follow-up.

Get Your Providers Billing Sooner

Credentialing delays hold revenue you’ve already earned the right to collect. Medicotech manages provider enrollment, CAQH maintenance, PECOS submissions, and payer follow up for practices across all 50 states. We’ll review your current credentialing files and give you a realistic timeline for each provider.

Frequently asked questions about insurance credentialing

How long does insurance credentialing take?

Plan on 90 to 150 days for most commercial payers in 2026. Medicare through PECOS runs faster, often 45 to 90 days for a clean electronic submission. Medicaid varies widely by state, roughly 60 to 120 days. Some large commercial networks and high demand specialties stretch past 180 days.

What documents do I need for insurance credentialing?

You need a current state license, individual and group NPI, DEA registration if you prescribe, a malpractice insurance certificate with current limits, board certification, medical school and residency diplomas, a gap free CV, a W-9, and government issued photo ID. Missing documents are the single largest cause of delay.

Can I bill insurance before credentialing is complete?

Usually no. Most payers pay only for services rendered on or after your contracted effective date. If claims are submitted before enrollment is complete, specialized denial management services can help identify payer issues, correct claim errors, and improve reimbursement outcomes. A few payers offer retroactive effective dates back to the application received date, but that’s a payer specific concession you must confirm in writing before you rely on it.

What is the difference between credentialing and payer enrollment?

Credentialing verifies that your license, education, training, and work history are real and current. Payer enrollment is the contracting step that follows, where the payer issues a participation agreement and an in network billing number. You need both before you can bill as an in network provider.

Do I need a CAQH profile for Medicare?

No. Medicare enrollment runs through PECOS, which is a CMS system and doesn’t read CAQH. Nearly every commercial payer does require an attested CAQH ProView profile, so build both at the same time rather than in sequence.

How often do I have to recredential?

Most commercial payers recredential every two to three years. Medicare revalidation runs on a three or five year cycle depending on your risk category, and CMS has shortened the cycle to three years for higher risk provider types. Licenses, DEA registration, and malpractice coverage all expire on their own separate schedules.

What is primary source verification?

Primary source verification means the payer or its credential verification organization confirms your credentials directly with the issuing body, not with you. Your state medical board confirms the license. Your residency program confirms training. Under current NCQA rules that verification data has a limited shelf life, so slow document collection can force a restart.

What happens if my credentialing application is denied?

Denials usually come from a closed panel, an unresolved malpractice or sanctions issue, or an incomplete file rather than a judgment on your competence. Closed panel denials can often be appealed with a network need argument showing patient access gaps in your area. Ask for the specific reason in writing before you respond.

Should I credential as an individual or under my group Tax ID?

If you bill under a group, you need both. The individual provider gets credentialed and the group holds the contract and the Tax ID that payments flow to. Skipping the group link is a common reason claims deny even after a provider is approved.

How much does insurance credentialing cost?

Outsourced credentialing typically runs per provider per payer. The larger cost is usually the revenue delay. A provider who could bill 40,000 dollars a month and waits an extra 60 days because of a document error loses far more than the service fee.

Which payers should I apply to first?

Start with Medicare, then your state Medicaid program, then your top three to five commercial payers by local patient volume. In most markets the top five payers cover 70 to 80 percent of potential revenue, so sequencing this way gets cash flowing months earlier than applying alphabetically.

Does telehealth require separate credentialing?

Not usually a separate credentialing track, but you must hold a license in every state where your patients are physically located at the time of service. Each additional state license adds its own primary source verification step, which is why multi state telehealth practices see longer timelines.

Getting credentialed without losing a quarter of revenue

The providers who get credentialed fastest aren’t the ones with better payer relationships. They’re the ones who collected every document before submitting, matched their NPPES and PECOS records exactly, authorized each payer in CAQH, and followed up every two weeks without waiting to be asked.